Put four monthly charts next to each other and you get one of the cleanest splits in global equities right now. The two largest economies in Asia are going nowhere. The two chip exporters are going vertical. GDP says one thing; the tape says the opposite — and the tape is the one with your money in it.

Market

Level

Day

The read

India — Nifty 50

23,989

+1.87%

Range-bound 18 months

China — CSI 300

4,884

−0.16%

Structural sideways decade

Taiwan — EWT

103.79

+0.98%

All-time high, parabolic

S. Korea — EWY

210.00

+2.03%

Vertical off a multi-year base

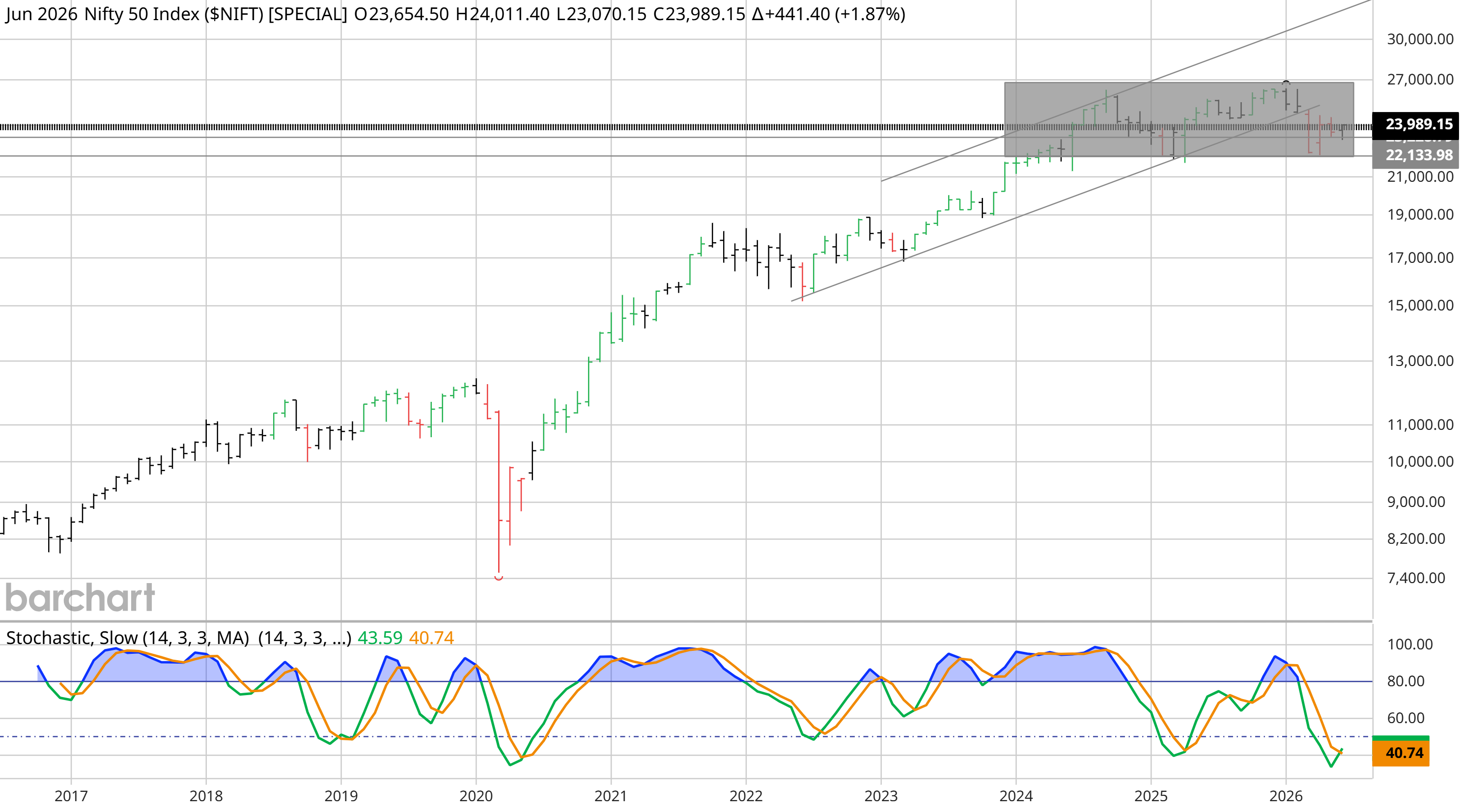

India — Nifty 50: a market resting, not leading

A spectacular bull run from ~8,000 in 2017, then nothing. For roughly the last 18 months the index has churned inside a box, about 22,100 to 27,000. The slow stochastic at 40.74 is rolling over — a market resting, not leading.

Figure 1. India — Nifty 50 ~23,989, resting inside an 18-month range. Source: Barchart (monthly).

C — free account

The free C account unlocks the full Daily Pulse — every section of this read.

One tap with Google or one email — no password, no card. You are

signed in until you sign out, on this browser, from then on.

Already joined on this browser? The full edition shows automatically —

if it doesn't, sign in again here. Looking for the archive, portfolios and

realtime? That is C+.